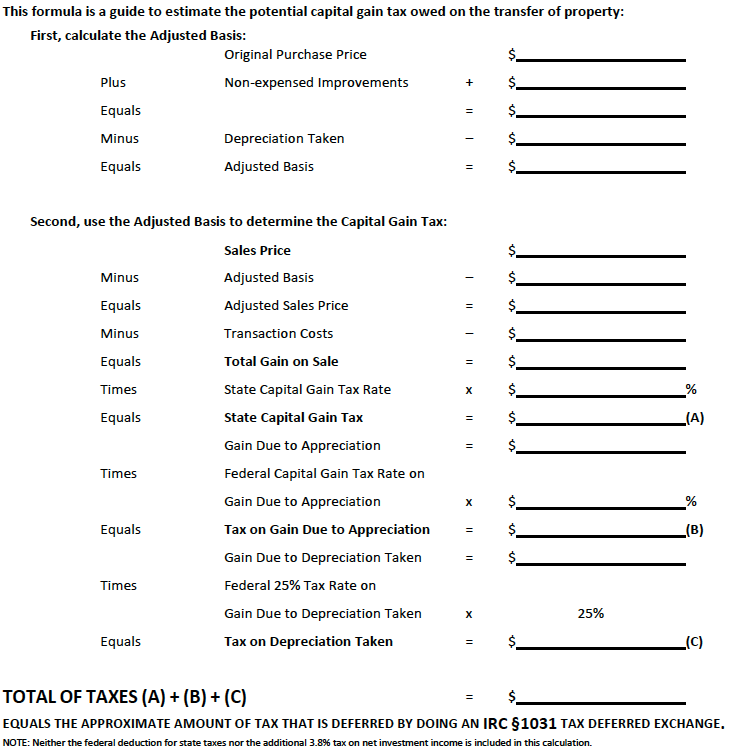

An Exchanger should always consult with competent independent legal and/or tax advisors to determine the applicability of any IRC 1031 tax deferred exchange benefits. The gain, not the profit or equity, from the transfer of investment property is subject to the combination of federal and state capital gain taxes and federal taxes on the gain due to the depreciation taken on the property. Remember, it is possible to have little or no equity in the investment property being transferred and still owe taxes!

CLICK TO DOWNLOAD ESTIMATING TAX DEFERRAL REFERENCE PDF

Read More:

Online Capital Gain Estimator

Online Exchange Days Calculator